Great Mortgages. The Right Insurance. Expert Advice.

The Bank of Canada Rate Cut – What Could It Mean For You?

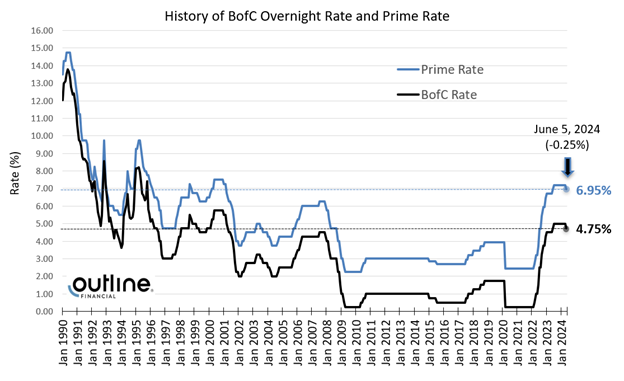

On June 5th, the Bank of Canada announced a much anticipated 0.25% decrease in its overnight lending rate, bringing the overnight rate to 4.75% and the prime rate to 6.95%. This is the first rate cut since 2020 and could signal more to come in 2024 and 2025.

What could this rate drop mean for you in the short and long term? We dive into the details below, or read our formatted report by clicking [here].

What Does This Rate Drop Mean For You?

If you have a variable rate mortgage with adjustable payments:

- You will see a decrease in your payment of about $15 per $100K of mortgage depending on your amortization.

If you have a variable rate mortgage with static/non-adjustable payments:

- The interest portion of your payment will decrease and more of the payment will go towards the principal (unless you have already hit your trigger point).

If you have a home equity line of credit:

- Your minimum payment will decrease by about $20 per $100K of HELOC balance.

If you have a fixed-rate mortgage:

- There is no immediate change, although it could positively impact your renewal options.

If you are currently shopping for a home or have a pre-approval?

- Your buying power may have increased. If your approval rate is reduced by 0.25%, it could increase your purchasing power by about 2.5%, all else being equal (i.e., if you were buying for $1,000,000, it’s possible you may now qualify for approximately $1,025,000).

- What if you have a fixed rate pre-approval? As fixed rates typically move in tandem with bond yields (which move in anticipation of a Bank of Canada rate change), the 0.25% drop by the Bank of Canada was already priced in most fixed rates. That being said, if we see a continued expectation of further rate reductions, expect bond yields to gradually decrease as the rate cuts become more imminent (this will be particularly true for shorter-term products).

What Does This Rate Drop Mean For You In The Longer Term?

Are higher home prices on the way?

- As rates drop, buying power increases. While the 0.25% rate reduction doesn’t make a huge mathematical difference, it could make a huge psychological difference to home buyers looking to beat the potential rush if rates fall further. As illustrated in the attached chart [click here], you can see that from April 2004 to April 2024, a reduction in interest rates has typically been followed by a period of increasing average prices within the Greater Toronto Area.

Is this the first of more rate cuts to come?

- The short answer? Yes, very likely. As of the time of writing, most economists & banks are projecting another 1.00% to 1.50% of rate reductions by the end of 2025. While the timing of future rate reductions is uncertain, if inflation continues to cool, and the economy stays in check, the Bank of Canada can continue its march downward. For reference, the Bank of Canada defines an overnight rate of between 2.25% to 3.25% as the “neutral rate” for the economy (i.e., an overnight rate that is neither expansionary nor contractionary for the economy). Given that the current overnight rate is 4.75%, there is potentially another 1.50%+ of rate reductions to go, to bring the overnight rate into neutral territory.

Fixed or Variable?

- As the overnight rate (and prime rate) drops, the potential attractiveness of a variable vs. fixed rate product grows. During March 2024, variable rate mortgages accounted for just over 12% of all mortgage originations. Expect this number to increase as the 10-year average is closer to 25%. Looking to weigh your options? At Outline Financial, we have developed a number of analysis tools to help quantify the pros, cons, costs, and benefits when comparing your fixed vs. variable options.

How Will This Impact Fixed Rates?

- As mentioned above, fixed rates are heavily influenced by government bond yields. Given that bond yields move “in anticipation of” a potential Bank of Canada rate change, the 0.25% rate reduction was already priced in most fixed-rate approvals. That being said, if we see a continued expectation of further rate reductions, expect bond yields to gradually decrease as the rate cuts become more imminent (this will be particularly true for shorter-term products).

Why Did the Bank of Canada Lower Rates?

While countless articles will be written about the June 5th Bank of Canada (BofC) rate cut, we’ve included some key takeaways below, along with links to the Bank of Canada press release as well as the opening statement from Tiff Macklem (Governor of the Bank of Canada).

Links to the press release and opening statement:

- Bank of Canada, June 5th press release [click here]

- Opening statement: Tiff Macklem (Governor of the Bank of Canada) [click here]

Why did the Bank of Canada decide now was the time to reduce rates?

- “With continued evidence that underlying inflation is easing, Governing Council agreed that monetary policy no longer needs to be as restrictive and reduced the policy interest rate by 25 basis points” – BofC press release

- “We’ve come a long way in the fight against inflation. And our confidence that inflation will continue to move closer to the 2% target has increased over recent months. The considerable progress we’ve made to restore price stability is welcome news for Canadians”. – Tiff Macklem opening statement

The Bank of Canada acknowledges further rate reduction may be on the way, but will take it one meeting at a time:

- “If inflation continues to ease, and our confidence that inflation is headed sustainably to the 2% target continues to increase, it is reasonable to expect further cuts to our policy interest rate. But we are taking our interest rate decisions one meeting at a time.”- Tiff Macklem opening statement

- “We don’t want monetary policy to be more restrictive than it needs to be to get inflation back to target. But if we lower our policy interest rate too quickly, we could jeopardize the progress we’ve made. Further progress in bringing down inflation is likely to be uneven and risks remain.” – Tiff Macklem opening statement

When are the next Bank of Canada rate announcements?

- July 24 – (Interest rate announcement and Monetary Policy Report)

- September 4 – (Interest rate announcement)

- October 23 – (Interest rate announcement and Monetary Policy Report)

- December 11 – (Interest rate announcement)

For more details about the 0.25% Bank of Canada rate cut, or to discuss which rate or product options might be right for you, please contact a member of the Outline Financial team as we are always on standby to help.